Fintech meets crypto #5

DAOs are here, FinOps is a thing and a few words about ultrasonic payments

Hi 👋

What a week that was!

This week’s edition is full of interesting stuff.

The weekly theme focuses on DAOs (Decentralized Autonomous Organizations) - if you want to stay up-to-date with the rest of the world, you need to know what DAO is.

I’ve collected also some amazing recommended reads

Welcome to “Fintech 🤝 crypto” - episode #5.

If you want to get new episodes directly into your mailbox, hit the button below:

Let’s go! 🚀

Weekly theme - DAOs 🤔

Last week something special happened ✨

ConsitutionDAO - a collective formed to buy a copy of the US constitution - has taken the crypto ecosystem by storm over the last 7 days.

🤔 What is ConstitutionDAO?

🤔 What is DAO?

🤔 What does it mean they wanted to buy a copy of the US constitution?

🤔 Why does it matter?

Let me unpack this for you.

Some basics first:

DAO - Decentralized Autonomous Organization - is a new type of organization that's decentralized (owned by many), and autonomous (can't be interfered with by outside actors.) It's created and run on the blockchain.

DAOs would not be functional without DeFI apps & tools they are using.

You can think of DAOs as web3 companies. These are organizations (made of people who own a particular DAO token) that are built to do something. Provide value. But they are decentralized - meaning there is no single point of authority. Token owners have voting rights and can decide on the future of a DAO. The more tokens you have, the more voting power you possess.

In DAOs, decentralization doesn’t mean every person is involved with every decision. It means anyone can be involved in decisions if they want.

If they are “like-companies”, how do they earn money? Good question. The simplest path is:

DAO can issue their token that people, who want to participate in this DAO, can buy. If the DAO does well, the token’s value will appreciate in time (just like traditional stocks). That is how the initial treasury is created 🏦

How the money is spent is up for voting. How DAO will develop itself is up for voting too. The proposals need to be first published and then DAO members can vote if they agree with them. There is no single point of authority that can decide on the future of DAO.

There are different types of DAOs:

Social DAOs (e.g. BanklessDAO, Rekt)

Investment DAOs (e.g. TheLao, PleasrDAO, Flamingo & ConstitutionDAO)

and other.

Here is a pretty neat comparison of web2 companies vs web3 DAOs 👇

And this is how current DAOs landscape looks like:

Pretty busy, huh?

To sum up: the DAO space is booming 💥

My prediction is that just like 2020 was a DeFI year, 2021 - NFTs, 2022 will belong to DAOs.

If you are interested in reading more about DAOs, I highly recommend any of these four articles:

👉 What are DAOs? Here’s what to know about the ‘next big trend’ in crypto

👉 DAOs: Absorbing the Internet

Alright, back to the ConstitutionDAO and their quest to buy a rare copy of the US Constitution at a Sotheby's auction.

Why the whole thing was so damn special?

ConstitutionDAO showed off one of Ethereum’s superpowers - that is, its ability to coordinate capital globally in an extremely rapid way. The DAO community was created in 3 days and in 7 days they went from $0 to over $40 million 🤯

To do this sort of capital formation in the traditional finance world, you’d have to use centralized payment processors, it’d be extremely slow, the money raised would be much less and the raise itself would be very exclusionary. You also couldn’t create a DAO out of it and have it be governed by token holders - the traditional system is just not set up to do this in any practical way.

Furthermore, thousands of people signed up for their first crypto wallets because of the hype around this project.

In the end, a hedge fund billionaire, Ken Griffin, outbid ConstitutionDAO and bought a copy of the US constitution for $43 million.

Look, this outcome wasn’t that surprising after all. Ken Griffin exactly knew how much money DAO had (before the auction started) and what was the maximum price they could pay.

TradFi won this time.

DeFI will strike back.

Happened last week 👀

1) N26, Germany’s most valuable fintech, withdraws from the US 🇩🇪🇺🇸

⏱ In short:

CEO and Co-Founder of N26, Maximillian Tayenthal, has just announced their shutting down of its US operations, less than two and a half years since it launched in the country. N26′s American customers will no longer be able to use its app from Jan. 11, 2022.

🧐 My comment:

Last month UK neobank - Monzo - withdrew U.S. banking license application, now N26 says resigns from US market. What is going on? Why is it so difficult for European fintechs to expand their services into America?

Officially, N26 withdraws from the US because they want to focus on their strategic, core European business, i.e. in Germany. Plus they are planning to expand into Eastern Europe amid growing demand in the region.

Unofficially - N26 had only 100k active users in the US (they claimed they had 500k) and it was extremely difficult for them to gain traction on the American market (which has 95% banking penetration, sic!).

Interestingly, it’s not the first time N26 has pulled its services from a major English-speaking market. The firm withdrew from the U.K.early last year, blaming the country’s exit from the European Union. N26 had reportedly been struggling to gain U.K. users.

The competition in the fintech space is huge and it’s not easy - even for big players in their countries, like Monzo or N26 - to expand to other regions, like North America, Asia, or LATM. That is exactly why the fintech market is geographically segmented. But this topic deserves a separate place in ‘weekly theme’ in one of the future editions of ‘Fintech meets crypto’.

2) EPI calls for public funding to support pan-European payments system 🇪🇺

⏱ In short:

The European Payments Initiative (EPI) is seeking public funding to support its development of a unified payment system across Europe that would compete with US-based networks such as Visa and Mastercard.

🧐 My comment:

EPI’s mission is to “is to create a unified payment solution tailored for Europe” and, as a result, become less dependent on US-based payments networks - Visa and Mastercard. That’s a noble mission. But is it achievable?

EPI has the support of over 30 banks and acquirers. They have already invested €30m in the initiative as of today. Several billions of euros more will be needed. €30m already invested are peanuts. And they still are far from launching even a PoC version of the system. That’s why they are calling for public funding (probably from the EU?).

There are two paths from here. The first - the EU throws a lot of money into EPI, involved banks & acquirers are over the moon, the future looks bright, and just after 5-7 years of meetings, agreements, and regulatory discussions EPI delivers something. Will it be groundbreaking by then? Will it involve most of the European banks? I doubt that. The second path is simpler and shorter. The EU will not fund this initiative and it will simply die.

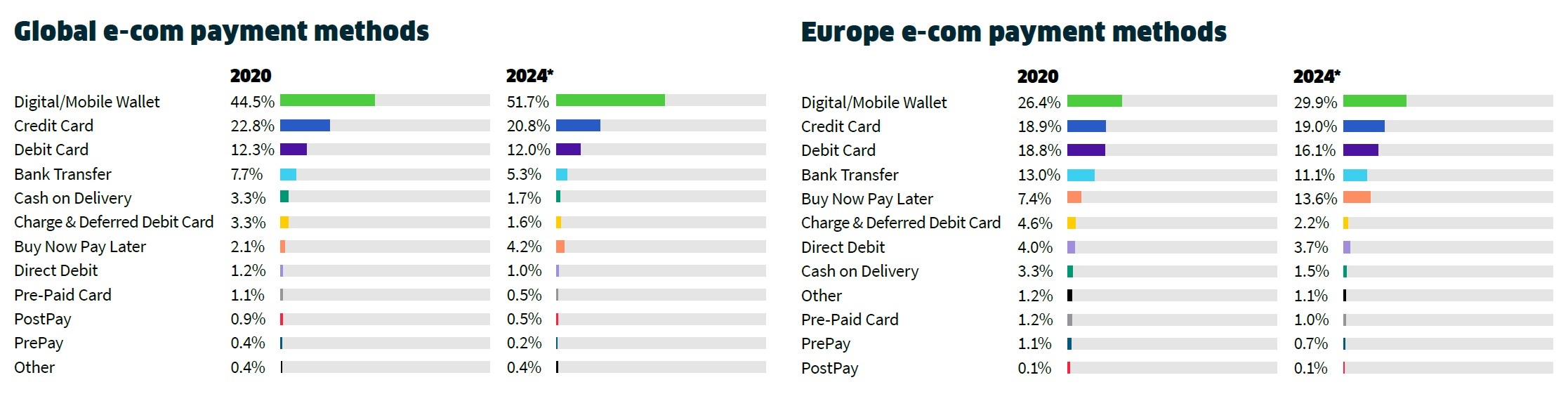

3) E-wallet use skyrockets in Europe 🚀

⏱ In short:

Pandemic did what we all expected it would do. It accelerated the growth of contactless & mobile payments across the globe. Just look at the numbers below:

🧐 Key points:

Digital/mobile wallets are definitely number 1 if we are talking about e-com payments methods. Both in Europe and globally. In 4 years, it is expected they will be used in 30% of e-com transactions (Europe) or in over 50% (globally). Wow.

Look at the numbers for Buy Now, Pay Later in Europe. 2x growth in years up to almost 14%. Klarna and other BNPL fintechs can sleep well.

What will decline? Credit cards, debit cards & bank transfers. No surprise here.

4) African payment apps to add ultrasonic authentication for contactless transactions 📱

⏱ In short:

Nigeria-based payment services provider - Paga Group - plans to add ultrasonic authentication to their payments apps and plans to roll it out as a contactless verification option to some 33,000 merchants and 19 million users across Africa.

🧐 My comment:

Do you know that it is possible to authenticate the user using sound instead of NFC? Yep, that’s right. It’s called ultrasonic data-over-sound proximity verification technology.

This authentication solution is a ‘person present’ authentication technology provided by US data-over-sound company Lisnr.

This technology probably will not dominate European or American payments markets but it’s a reasonable solution for underdeveloped markets where NFC-ready equipment might not be that common.

BTW, some analysts predict that data-over-sound is the future of frictionless data transmission - especially between IoT devices.

5) Sotheby’s auction thrusts Ethereum into the mainstream 💥

⏱ In short:

Sotheby’s fielded real-time bids denominated in Ethereum for two Banksy pieces of artwork.

BTW, the guy running the auction definitely owns it ❤️

🧐 My comment:

A huge step for ETH and the crypto world. This is how cryptocurrencies are entering the mainstream. NFTs, EFTs, crypto payment cards (by Visa and Mastercard), and now auctions. We will see more in 2022.

Great reads worth your time 📚

📕 How to Move Money in the 21st Century (by Seema Amble and David Haber)

Really interesting piece on “financial operations” (FinOps) - emerging software category with a massive opportunity to rethink the way businesses manage their money.

The main thesis is: there are two money movements workflows - Payins & Payouts. Both are manual today. This can be improved.

The article gives a nice overview of the current situation and tries to answer an important question: what type of FinOps products can be built to solve this problem?

📗 The default banking-as-a-service platform will be developer-first (by Ayo)

This one is from 2020 but it’s definitely worth reading now. It gives a great explanation why fintech startups should be developer-first, not sales-first - especially if they want to be “a default choice” for other startups.

To be the default; to be the company that the mythical two people in a garage choose to use, or that someone building a side project on the weekend chooses to use, onboarding must be developer-first; a developer must be able to issue, fund and transact on a card or bank account without talking to a human at your company.

The article focuses on the issuing part of the business which is still less crowded than the acquiring/PSP part of the fintech ecosystem.

A great read for all fintech geeks. Thank you @KamilSindi for sharing this one with me!

📘 Debit cards are hidden financial infrastructure (by Patrick McKenzie)

Two weeks ago in “Fintech meets crypto #3” I recommended you another article by Patrick - it was about credit cards. Last week he wrote the next one and this time the focus is on debit cards.

If you want to understand why debit cards are crucial and indispensable for banks (to the surprise of many), go and read it.

📙 Payments, Payment Rails, and Blockchains, and the Metaverse (by Matthew Ball)

Oh boy, Matthew can write, can’t he? This piece is a 15min read but it’s worth it.

It’s the part VII (sic!) of Matthew’s “The Metaverse Primer”.

It focuses solely on payments methods, payments rails, and services. First, it gives an amazing overview of the current payment ecosystem and then describes how payments can be done in a metaverse economy.

If you have no clue what metaverse is, go and read this.

Gold Tweets 🏅

It’s almost 2022 but talking with people who think that “crypto is bitcoin and it’s bad” is still problematic and challenging. I know it from my own experience. Here is a great thread by Chris on how to talk to your friends & family so they may become interested in this space:

You can use this thread to pitch your TradFi friends:

And three more:

That’s all for now 👋

Next episode - next Tuesday. Have a great week everyone!

Remember, if you're enjoying this content, please do tell all your fintech and crypto friends to check it out and hit the subscribe button.

Feel free to reach out to me:

Twitter: @pawt

LinkedIn: linkedin.com/in/paweltrybulski/

Stay curious,

/Paweł